Navigating Rates

Populism: would markets vote for it?

Populists may excite many voters, but markets often aren’t fans of the higher spending, inflation, and lower growth their policies tend to bring.

KEY TAKEAWAYS

- We see reasons why populism is set to remain a key feature of politics and potentially influence the outlook for some economies in the foreseeable future.

- Income inequality and opposition to immigration have fuelled a sense of social injustice among some voters, stoking support for populism.

- Our research shows markets tend to perform poorly over the longer term when populist policies are adopted.

- Under populist governments, we found a mixed performance for fixed income, underwhelming results for equities and weaknesses for currencies.

Populist talk has been everywhere during a busy year for elections. From former US president Donald Trump’s pledge to pursue “America First” trade policies to France’s left- and right-wing parties’ plans to reduce the pension age, populism has been front and centre on campaign trails. So, what are the implications of populism for investors?

In summary, our research shows markets tend to perform poorly over the longer run when populist policies are adopted. But what is populism? Political scientist Cas Mudde describes populism as a “thin-centred ideology” that considers society to be split into two, the “pure people” and the “corrupt elite”, and which argues that politics should be an expression of the general will of the people. 1

A common feature of all populist parties, whether on the left or right, is their anti-establishment agenda, often centred around a strong leader sometimes characterised as giving a voice to popular opinion neglected by other parties. Most are inclined towards nationalism – identifying strongly with their nation and its interests – and against globalism. The vote by the UK in 2016 to exit the European Union and the election of Mr Trump as US president the same year are often seen as populism’s high-water mark.

We think understanding populism as a political force is critical to positioning portfolios actively in a changing landscape.

Populism may be gaining ground

The share of populist governments has risen since the early 1980s. Globally, the populists’ vote share hit around 25% just before the Covid-19 crisis.2 Populism’s ascent since has been less clear. In India, Narendra Modi – often described as a populist – has been sworn in for a historic third term as prime minister – but with a weakened majority. In France’s recent election, a left-wing coalition thwarted the far-right National Rally’s (RN) bid for power. But the RN and other populists, on the left and right, made gains in June’s European elections. And in September, Alternative for Germany (AfD) triumphed in a vote in the German state of Thuringia, the first time a far-right party has won a regional election in the country’s postwar period. The new populist Sahra Wagenknecht Alliance (BSW) also did well in the votes in Thuringia and Saxony.

In the US, political polarisation has risen in recent years. Mr Trump is often – rightly – seen as embodying contemporary US populism. However, the current US administration under President Joe Biden has continued the tough stance on trade with China. November’s presidential election between Mr Trump and Vice President Kamala Harris remains a close call.

We see reasons why populism is set to remain a key feature of politics and influence broader political thinking for the foreseeable future.

Inequality and immigration are key to populism’s rise

Among a myriad of reasons for populism’s support in recent years, we think two factors play a significant role:

1. Inequality: globalisation and the automation of production processes has created bigger gaps between the richest and poorest in advanced economies since the 1980s. But while income inequality has actually edged down in the past ten years or so in many countries, wealth inequality has continued to rise.

2.Immigration: the fear of losing out economically to immigrants has gained ground among some voters in Europe during the past decade or so. Many of those also fear a loss of cultural identity.

More recently, the cost of funding the war in Ukraine and the green transition were cited by political observers as additional reasons for the far-right’s popularity in the European elections.

Memories of the global financial crisis also linger when government bailouts were provided to banks at great cost to economies. Some euro area periphery economies also received support during the European debt crises. For some voters, that support triggered a lasting sense of unfair treatment.

Still, none of the above factors can fully explain the increased support of populists. Hence, it’s also important to acknowledge the influence of false claims across social media in fuelling a sense of social injustice, as well as the loss of collective memories of hard times during dictatorships and wars.

Economic impact: sugar rush then hangover

Academic research suggests economic growth tends to suffer significantly under populist governments.3 Economic growth can be between 0.6 and 1 percentage points lower per year in the five to 15 years following the instalment of a populist government. True, populists tend to stimulate their economies through higher spending and lower taxes initially – but the drag on growth typically starts two to three years later:

- International trade tends to fall as populists put the interests of their economies first and hike tariffs.

- Government debt-to-GDP ratios climb as spending rises – usually slowing growth in the long run.

- Inflation increases as demand stimulus grows and international trade falls.

- Freedom tends to contribute to greater prosperity, research suggests.4 Research also shows freedoms like political rights and civil liberties can be eroded under some extreme populist governments.5

Market impact: disappointing results

Our research focused on how financial markets performed in the long run after a populist becomes the head of a government.6 We analysed median real (inflation-adjusted) returns (all in USD) for the three, five, 10 and 15 years from the year that a populist government came into office, even when that government did not remain in power over the entire period and compared the results to the long-term real returns of financial markets.7

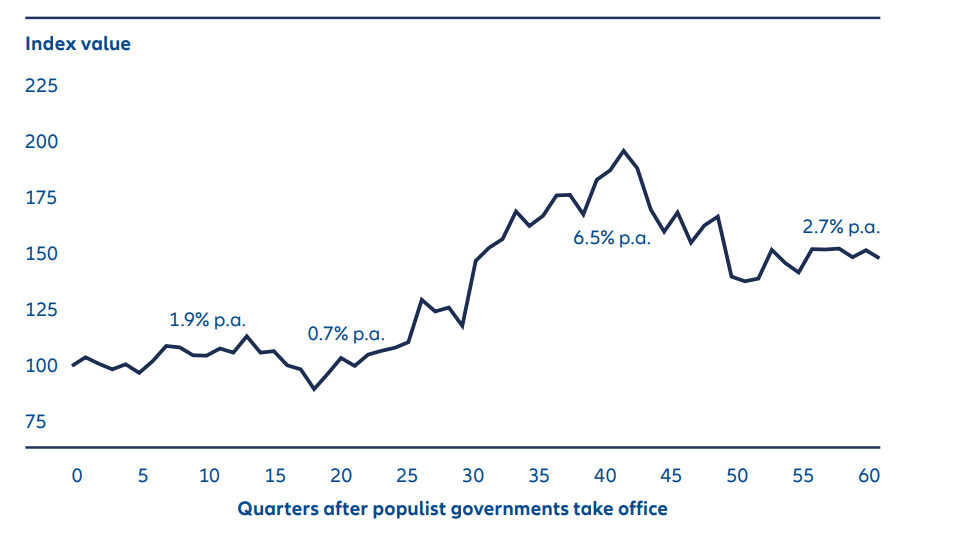

1. Fixed income: higher debt can mean lower returns

Annual bond performance under populists in the first three years was 1.9%, around the same as long-term global bond market performance. Performance slipped over the five years, with the 0.7% returns lower than the long-term bond average (see Exhibit 1). The rise in the public debt-to-GDP ratio under populists tends to weigh on bond returns.

Although returns over 10 and 15 years were higher than the median long-term market performance, the results are somewhat skewed by the inclusion of several populist governments between the 1990s and just before the Covid-19 pandemic when global bond markets did well.

Exhibit 1: Bond performance is mixed once populists come to power

Source: Allianz Global Investors (own calculations), LSEG Refinitiv, GFD. Quarterly data as at Q4 2023. Legend: populists as defined by Funke, Schularick, Trebesch. Note: performance has been calculated starting from the year that populists came to power until 20 years thereafter, even when populists have not been in power for the entire time span.

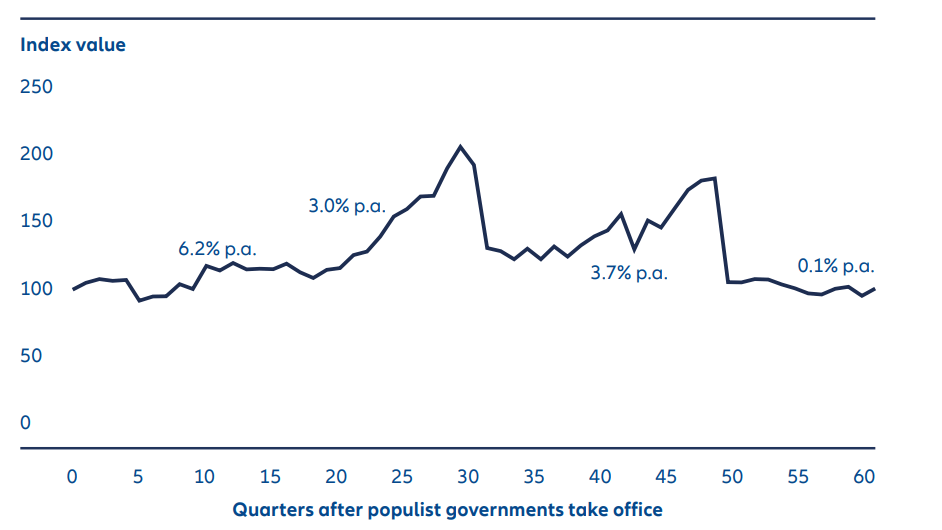

2. Equities: underwhelming performance in the longer term

Equity returns were solid in the first three years (around 6% a year), but weak in the years afterwards, falling close to 0% annually over 15 years, (see Exhibit 2). This compares with long-term US equity returns of close to 7% and non-US equity returns of close to 5%.

We see the underwhelming performance in line with the negative longer-term hit to economic growth. The initial steadiness in equities is consistent with the expansionary fiscal policy pursued by populists and the stable economic growth rate in the first two to three years under a populist government.

Exhibit 2: Long-term equity performance is disappointing under populists

Median inflation-adjusted equity return index (in USD) in advanced economies after 1900

Source: Allianz Global Investors (own calculations), LSEG Refinitiv, GFD. Quarterly data as at Q4 2023. Legend: populists as defined by Funke, Schularick, Trebesch. Note: performance has been calculated starting from the year that populists came to power until 20 years thereafter, even when populists have not been in power for the entire time span.

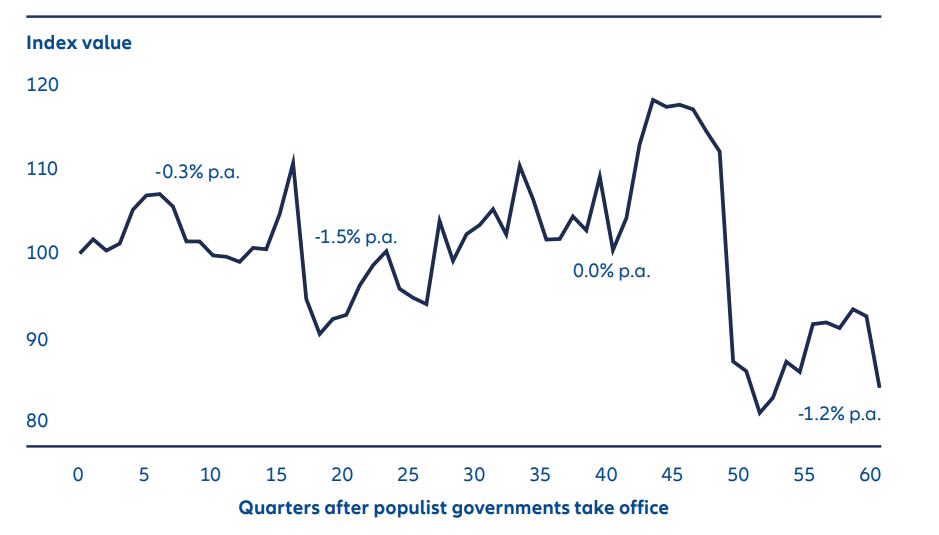

3. FX: lower growth weighs on currencies

Our analysis found currencies tend to fall in real terms in the long run (see Exhibit 3). We think the combination of lower growth, higher inflation, higher government debt and less financial openness often weighs on currencies.

Exhibit 3: Currencies tend to depreciate under populists in the long run

Source: Allianz Global Investors (own calculations), LSEG Refinitiv, GFD. Quarterly data as at Q4 2023. Legend: populists as defined by Funke, Schularick, Trebesch. Note: performance has been calculated starting from the year that populists came to power until 20 years thereafter, even when populists have not been in power for the entire time span.

Investment factors to consider under populists

We see three themes investors should watch for when populists come to power:

1: More inflation and lower earnings from deglobalisation

Populists tend to reject the belief that greater economic integration is beneficial. They generally favour higher tariffs and other trade barriers, which can push up inflation. Deglobalisation leads to less productivity growth in the long run, as access to productivity-enhancing technology is hampered.

Inflation may also become more volatile as prices become more linked to local supply and demand, rather than international trade markets. Higher inflation and higher inflation volatility point towards lower equity multiples, as our work shows.

Deglobalisation also carries implications for labour markets. Less immigration implies a narrower labour supply and, as a result, more bargaining power for workers. Higher pay could fan inflationary pressures, drag on corporate margins and provide a headwind to equity and bond valuations.

2: Higher interest rates and a potential bond market reckoning

More profligate government policies can push interest rates up. In our view, such a scenario increases the likelihood of interest rates staying higher than under a non-populist government.

A government spending splurge raises the risk of re-pricing of bond markets, generally a gradual process. But re-pricing may be rapid – as was the case during former UK Prime Minister Liz Truss’s short-lived time in office in September 2022 when planned tax cuts caused bond market turmoil.

3: The country factor comes into play again

Populist governments tend to prioritise their domestic economy by boosting spending and raising trade barriers in an effort to protect homegrown businesses. For investors, that means more careful scrutinisation of politics within a country when selecting assets.

Active management can help negotiate a populist world

The rise in populism is a clear signal from voters who feel left behind by globalisation. However, populists often fail to improve inequality and can undermine economic growth and market performance in the long run. For sure, other factors – notably valuation and structural growth trends – remain important for long-term investors. But populism must be reckoned with rather than dealt with passively because it can present upheaval. Active managers who understand the economic dimensions of politics can help investors take advantage of the opportunities and manage the risks associated with this powerful political force.

1. The Populist Zeitgeist, by Cas Mudde, Government and Opposition, Volume 39, Issue 4, 2004.

2. Populist Leaders and the Economy, by Manuel Funke, Moritz Schularick and Christoph Trebesch, American Economic Review, December 2023

3. Populist Leaders and the Economy, by Manuel Funke, Moritz Schularick and Christoph Trebesch, American Economic Review, December 2023

4. Democracy Does Cause Growth, by Daron Acemoglu, Suresh Naidu, Pacual Restrepo, James A. Robinson, Journal of Political Economy, January 2019

5. FIW_2024_DigitalBooklet.pdf (freedomhouse.org); Populist Leaders and the Economy, by Manuel Funke, Moritz Schularick and Christoph Trebesch, American Economic Review, December 2023.

6. We followed the definition of populist governments used by Manuel Funke, Moritz Schularick and Christoph Trebesch.

7. After a change in government, it often takes several years to unwind decisions taken by previous administrations. Therefore, policy changes can have an impact over a long period. Our approach follows that of Manuel Funke, Moritz Schularick and Christoph Trebesch.